Ultimate Beneficial Ownership (UBO) refers to the persons or entities that are the ultimate beneficiary of a company. UBO also refers to situations in which ownership or controls are exercised through a chain of ownership, and by means other than direct control.

The European Union’s Fourth Anti-Money Laundering Directive (4AMLD) substantially addressed Ultimate Beneficial Ownership — by stipulating persons who have a share, voting rights or control of more than 25% are classed as Ultimate Beneficial Owner.

Additionally, 4AMLD determined that senior managing officials are treated as Ultimate Beneficial Owners, in cases where the above Ultimate Beneficial Owner criteria cannot be determined.

Finally, 4AMLD stipulates that European Union countries require entities in their jurisdiction to keep up-to-date ownership information. This takes the form of a central registry that is accessible to authorities, obliged entities, and public persons with a legitimate interest in determining Ultimate Beneficial Owner’s.

A Brief History of Ultimate Beneficial Ownership (UBO).

Ultimate Beneficial Owners and Financial Crime have been connected since the late 1980s. The connection between the two was first flagged in 1988 by the Bank for International Settlements. The bank created the first international instrument to focus specifically on Anti-Money Laundering (AML). The focus on ultimate beneficial owners continued to the 1990s.

With the 1990s starting with 40 recommendations proposed by the Financial Action Task Force (FATF), an objective from those recommendations was to combat the ability to disguise beneficial owners. This prime focus on Ultimate Beneficial Owners and AML continued to the turn of the millennium with the major G7 economies developing initiatives to combat the growing abuse of corporate AML.

It wasn’t until May 2000 when major economies required shareholders and directors to submit up-to-date information was not necessarily useful in declaring Ultimate Beneficial Ownership.

Despite years of global hunger to improve standards relating to beneficial owners, it was only in 2015 when genuine action was implemented to tackle the problem surrounding Ultimate Beneficial Owners. As it was in 2015 when, Transparency International (TI), published a report benchmarking the progress the G20 had made in improving transparency around beneficial ownership.

The report outlined that the UK was the only country rated as having a strong legal framework of the Ultimate Beneficial Owners of assets and companies. Most importantly, 2015 and 2019 brought 4AMLD and 5AMLD, which produced the most important changes to UBO regulations.

Implementation of 5MLD and Ultimate Beneficial Ownership (UBO) Registers.

As previously reported, the Fifth Anti-Money Laundering Directive (5AMLD) entered into force on 9 July 2018 with an implementation deadline of 10 January 2020. 5AMLD imposes additional obligations with regards to UBO, particularly on those in the finance and legal sectors.

Among the changes introduced by 5AMLD is a further requirement and tighter enforcement of 4AMLD, and to ensure process and controls are in place to provide broader access to European Member State’s central registries for beneficial ownership of corporate entities.

Under 5AMLD, these registers should allow access to the general public without the need for them to show a ‘legitimate interest’. In the UK, this registry would be Companies House.

Full implementation of 5AMLD and UBO is set to be delayed until 2021. However, Credas has always anticipated changes in the legislative and regulatory landscape and have now launched a FREE UBO solution — for all annual subscription customers.

Our Step-by-Step Process for Checking Ultimate Beneficial Ownership (UBO).

What specific policies and procedures should you be following concerning UBO?

You need to adhere to specific regulatory and compliance requirements for each country your organisation operates.

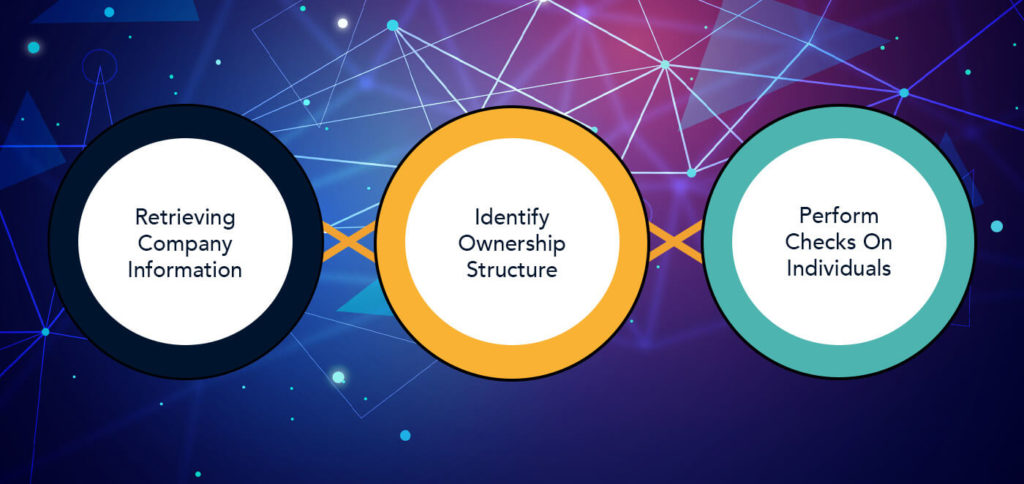

Here are Credas’ three steps that you need to implement to create an effective UBO program — which is now available via the Credas platform.

Step 1 — Retrieving Company Information

The first step in the process is to identify and verify an accurate company record. In the UK, this would be through a UK company registration number — via the companies’ house website. This record can include information such as company name, address, status, and key management personnel.

Whilst Companies House does hold details of directorships, Credas will displaying is the list of Persons of Significant Control, as held by Companies House.

While the specific information we collect is for UK based companies, the information you require depends on the jurisdiction and your compliance process and fraud prevention standards.

The key benefit of using our solution is that through a single company number, we can return the entire ownership hierarchy, regardless of how many parent companies the company you search may have.

Step 2 — Identify Ownership Structure and UBOs

The percentage you need to use to determine entities or persons who have an ownership stake in an organisation is down to your jurisdiction or compliance process.

While the Companies House register does not provide percentages, the legislation specifies you that calculating the total ownership stake, or management control, of any persons or entities, if it crosses the threshold for Ultimate Beneficial Owner reporting.

Step 3 — Performing Checks on Individuals

Once you’ve determined all individuals that are Ultimate Beneficial Owners, your due diligence process may require you to perform an Anti-Money Laundering or Know Your Customer check.

With Credas, this check can be performed directly from the company tree view, and the results will appear in real-time next to the Ultimate Beneficial Owner’s name.

Conclusion

While these three steps seem simple, in practical terms, without a proper system in place to check Ultimate Beneficial Owners, you are adding substantial strain on resources, costs, and delays to both your compliance teams and customers.

While technically possible, manual-based systems with employees performing individual searches on multiple registrars, and importing/storing data in line with GDPR, and tracking any changes to records, all with the experience to use that information to perform complex reviews is prime for risk and issues.

Manual processes are prone to errors, as every touchpoint is a potential mistake that could be costly while slowing down the onboarding or monitoring process for clients.

Credas’ solution streamlines Ultimate Beneficial Ownership checks in real-time and allows you to efficiently run AML and KYC checks against individuals, providing up-to-date, real-time information that can help supercharge your due diligence and compliance workflow.

Credas’ UBO solution links and handles information across multiple company structures, avoiding the duplication of effort, time and costs.